From Cost Tracking to Cost Management (FM – AECOO)

Transforming Facilities Investment Through Data Precision

Executive Summary

Most real property owners, facilities managers (FM), and design/build teams operate in a paradigm of cost tracking rather than cost management. While tracking records what has been spent, it does little to influence future outcomes, optimize decision-making, or ensure value delivery.

Transitioning from cost tracking to cost management is essential for optimizing financial outcomes.

This white paper notes that true cost management requires the use of current, verifiable, granular, standardized, and objective cost data for repair, renovation, maintenance, and new construction. Critically, this data must be separated from contractor overhead and profit (O&P) to enable transparency, comparability, and strategic control.

Understanding the shift from cost tracking to cost management allows organizations to unlock potential savings.

Organizations that rely on historical costs, national average cost data and location factoring, or lump-sum pricing models expose themselves to cost escalation, inefficiency, and loss of negotiating leverage. In contrast, those adopting a data-driven cost management approach gain predictive control, improved procurement outcomes, and measurable best value.

When organizations focus on moving from cost tracking to cost management, they foster a culture of proactive financial stewardship.

![]()

1. The Industry Problem: Cost Tracking vs. Cost Management

The distinction between cost tracking and cost management is crucial for effective resource allocation.

1.1 Cost Tracking Defined

Cost tracking is the retrospective recording of expenditures. It answers the question:

Effective cost management transcends basic cost tracking by incorporating predictive analytics.

“What did we spend?”

Typical tools include: – Financial reporting systems – Budget vs. actual comparisons – Historical project cost archives

While necessary for accounting and compliance, cost tracking is inherently reactive.

1.2 Cost Management Defined

Investing in training can aid teams in understanding the nuances of transitioning from cost tracking to cost management.

Cost management is the proactive control of costs throughout the asset lifecycle. It answers:

“What should this cost, and how do we ensure it does?”

It requires: – Current and forward-looking data – Real-time validation – Decision support tools – Transparent cost structures

1.3 The Gap

Most organizations attempt to manage costs using tools designed for tracking. This mismatch leads to: – Overreliance on outdated or irrelevant data – Acceptance of opaque pricing structures – Limited ability to challenge contractor pricing

It’s vital to recognize the difference between merely tracking costs and implementing effective cost management strategies.

2. Limitations of Traditional Cost Approaches

2.1 Historical Cost Data

Historical data reflects past conditions, not current realities. Market volatility, labor changes, and material cost fluctuations render such data unreliable for forward planning.

2.2 National or Regional Averages

Cost databases based on averaged data obscure local variability and project-specific conditions. These datasets: – Lack granularity – Mask real cost drivers – Require error prone location factors

2.3 Cost Factoring and Indexing

Applying escalation factors or location indices introduces compounding uncertainty. Each adjustment layer increases the margin of error.

Many firms still struggle to separate cost tracking from the advanced methodologies required for true cost management.

2.4 Lump Sum Pricing

Lump sum quotes: – Obscure underlying cost components – Prevent benchmarking – Embed unknown risk premiums

This approach shifts control from the owner to the contractor.

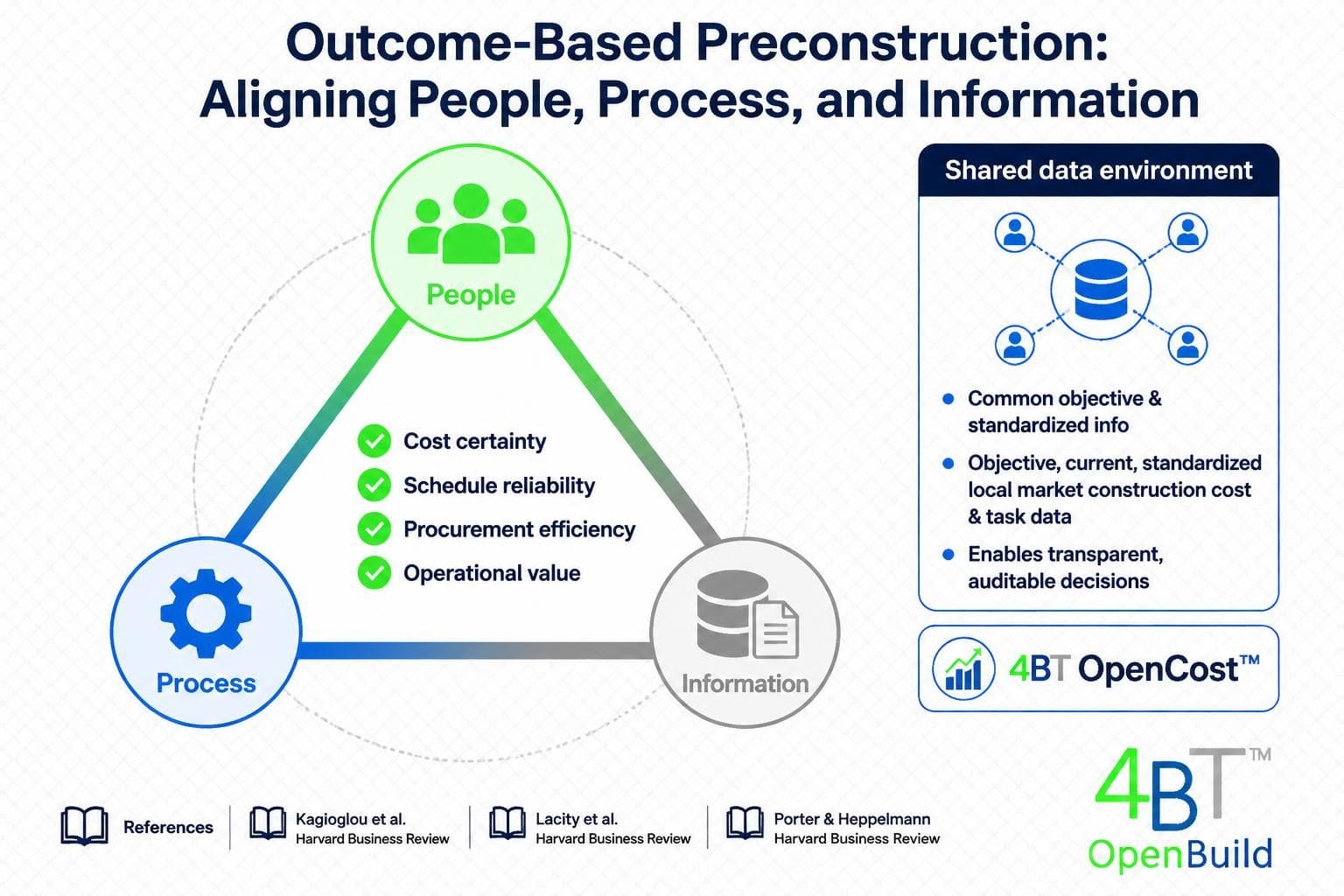

3. The Foundation of True Cost Management

Effective cost management is built on five key attributes of data:

Adopting a framework for transitioning from cost tracking to cost management can significantly enhance project success.

3.1 Current

Data must reflect real-time market conditions.

3.2 Verifiable

Each cost element must be traceable and auditable.

3.3 Granular

Costs should be broken down to unit-level components (labor, material, equipment), with associated productivity information.

3.4 Standardized

Uniform structure enables comparison across projects and time (e.g. expanded CSI Masterformat)

3.5 Objective

Data must be independent of contractor influence and free from embedded profit and overhead.

4. Separating Cost from Price: The Role of O&P

By understanding the role of accurate data, organizations can improve their transition from cost tracking to cost management.

A critical distinction exists between cost and price.

- Cost: Direct expenses for labor, materials, and equipment

- Price: Cost plus overhead and profit (O&P)

Most industry practices conflate the two, limiting transparency.

4.1 Why O&P Separation Matters

Removing O&P from baseline cost data allows: – Apples-to-apples comparison – Objective validation of contractor proposals – Flexible procurement strategies

4.2 Implications for Owners

Owners gain the ability to: – Negotiate O&P independently – Benchmark performance – Reduce contingency padding

5. Applications Across the Asset Lifecycle

5.1 Repair and Maintenance

Granular cost data enables: – Accurate work order pricing – Elimination of inflated service costs – Improved budgeting accuracy

Granular data aids in the shift from cost tracking to cost management by promoting precision in financial planning.

5.2 Renovation and Modernization

Detailed cost breakdowns support: – Scope validation – Value engineering – Real-time cost control

5.3 New Construction

Cost management enhances: – Design-to-budget alignment – Early-stage estimating accuracy – Risk reduction

6. Strategic Benefits of Cost Management

Organizations that transition from tracking to management achieve:

6.1 Predictive Control

Ability to forecast costs with confidence

6.2 Procurement Leverage

Improved negotiating position through data transparency

6.3 Cost Reduction

Elimination of unnecessary markups and inefficiencies

6.4 Performance Accountability

Clear metrics for contractor evaluation

6.5 Best Value Delivery

Alignment of cost, quality, and performance outcomes

7. Implementation Framework

7.1 Establish a Standardized Cost Database

- Unit-based pricing

- Trade-level detail

- Regular updates

7.2 Integrate with Procurement Processes

- Use data to validate bids

- Require cost breakdowns

7.3 Train Stakeholders

- Educate FM teams and procurement staff

- Align internal processes

7.4 Leverage Technology

- Digital estimating platforms

- Real-time data integration

8. Conclusion

The transition from cost tracking to cost management represents a fundamental shift in how organizations approach facilities investment. By adopting current, verifiable, granular, standardized, and objective cost data—independent of overhead and profit—owners can move from passive record-keeping to active financial control.

Ultimately, the evolution from cost tracking to cost management is not just beneficial; it is critical for maintaining competitive advantage.

In an era of increasing cost pressure and accountability, this shift is not optional. It is essential for achieving best value and long-term asset performance.

“You cannot manage what you cannot see.

Granular, objective cost data transforms spending into strategy.”

Fourt BT, LLC exclusively provides current locally researched, standardized, verifiable cost data spanning repair, renovation, maintenance (including preventive maintenance), and new construction.

References (Harvard Style)

Ashworth, A. and Perera, S. (2018) Cost Studies of Buildings. 6th edn. London: Routledge.

Eastman, C. et al. (2011) BIM Handbook: A Guide to Building Information Modeling. 2nd edn. Hoboken: Wiley.

Ferry, D. and Brandon, P. (2013) Cost Planning of Buildings. 8th edn. Oxford: Wiley-Blackwell.

Kirkham, R. (2007) Ferry and Brandon’s Cost Planning of Buildings. Oxford: Blackwell.

Smith, J. (2014) ‘The role of cost data in construction procurement’, Journal of Construction Engineering and Management, 140(5), pp. 1–9.

U.S. Government Accountability Office (GAO) (2020) Cost Estimating and Assessment Guide. Washington, DC: GAO.