Sustainable Asset Management Framework for the Federal Sector Built Environment

A sustainable asset management strategy for federal sector facilities requires…

-

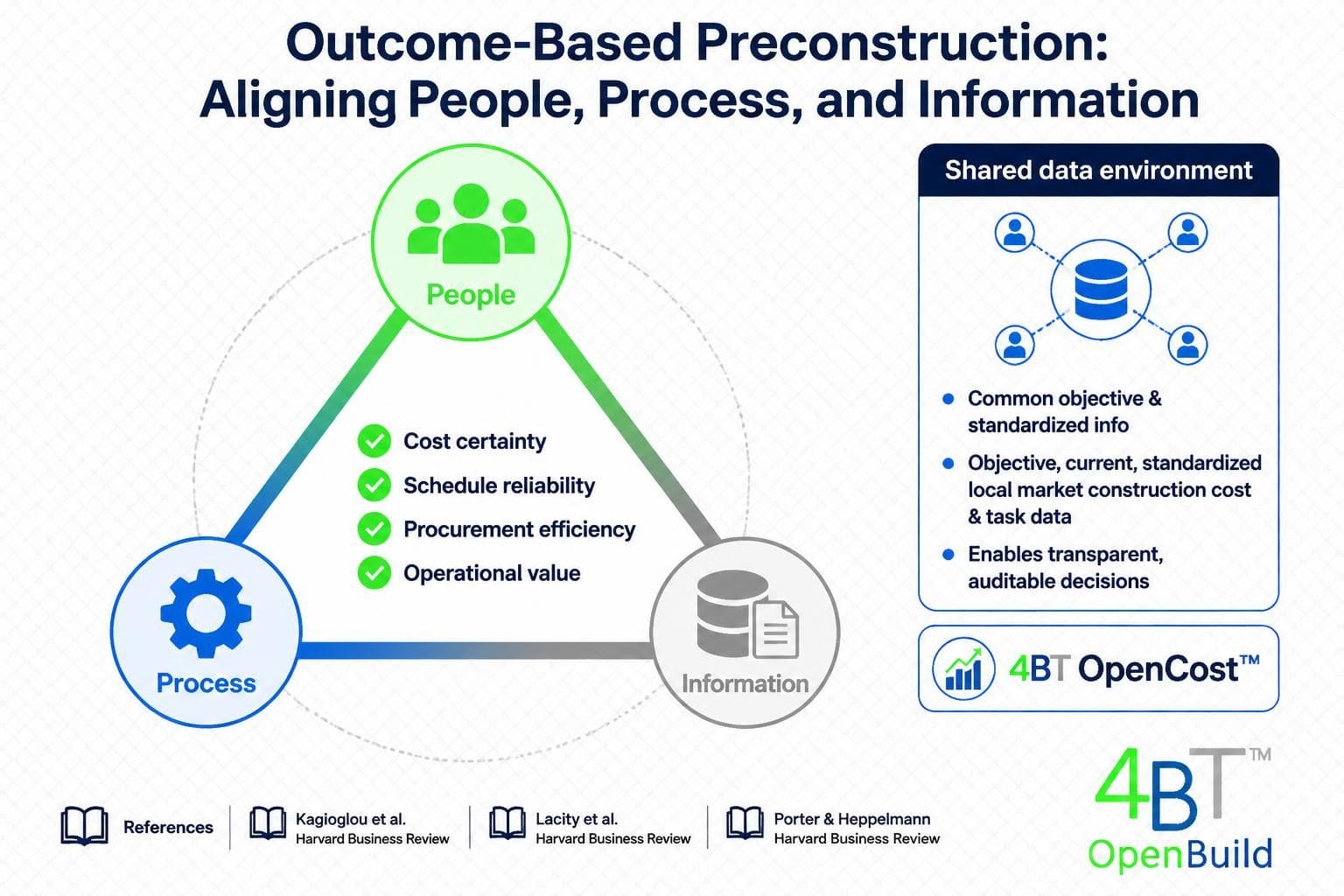

Addressing deferred maintenance requires focus upon People → Process → Information → and enabling Technology (PPIT).

-

Actionable cost data must be verifiable, granular, standardized, current, and locally researched (no market averages or passive location‑factoring).

-

Discontinuing customized “government developed” mandated technology systems that lack robust cost‑management functionality (e.g., documented failures of SMS Builder–style implementations); and shifting to interoperable systems and the exclusive procurement of proven commercial off-the-shelf solutions.

Problem statement

-

Deferred maintenance liabilities have grown dramatically across federal, state, and local portfolios; DOD and federal civilian building estimates rose from US$171bn (FY2017) to US$370bn (FY2024) (GAO 2025). Existing audits repeatedly identify root causes in people, process, information, and technology domains (GAO 2014; GAO 2018; GSA OIG 2021–24), and resulting high levels of financial and environmental waste.

-

People: leadership gaps, lack of training/certification for assessors, insufficient cross‑functional decision teams (GAO 2018; GSA OIG 2021).

-

Process: insufficient asset‑management plans, budgets that fail to separate sustainment vs backlog remediation, ineffective prioritization and disposal processes (NRC 1998; GAO 2014).

-

Information: poor inventory quality, duplicate/inaccurate records, inconsistent utilization reporting, and reliance on non‑actionable costing approaches (FASAB 2012; GAO 2018).

-

Technology: underused or misconfigured asset‑management systems, as well as waste when agencies repeatedly mandate or develop in‑house tools that do not meet cost‑management requirements (OMB 2022; ITAP 2023; Smith et al. 2024).

Solutions

Focus upon cost visibilty and cost management and information-based decision-making.

-

All backlog and sustainment estimates/costs/budgets must use actionable cost data that meet five tests:

-

Verifiable — each line item must be derived from primary source documentation (local labor, material, and equipment costs based upon current commerical standards),

-

Granular — cost broken down to trade/component, unit quantities, labor hours, and material unit prices.

-

Standardized — common schema (unit codes, measurement rules, contingency and overhead rules) across the portfolio to enable “apples to apples” comparison and audits.

-

Dynamic data that is continuously updated.

-

Locally researched — derived from local market information vs. ” national market average” cost data and location‑factor multipliers as primary inputs.

-

-

Rationale: Market averages and generic location factoring obscure real local cost drivers (labor availability, freight, regional trade practices) and materially misstate backlog/deferred maintenance valuations—leading to underfunding or misallocation (Fruin & Smith 2017; Harrison et al. 2019; O’Connell & Patel 2020).

Guidance on avoiding market‑average and location‑factor pitfalls

-

Treat national indices as secondary cross‑checks only; primary estimates must be sourced locally.

-

Require periodic local cost‑library refresh (at defined cadence, e.g., quarterly in volatile markets).

-

Use small‑sample competitive procurements (pilot procurements) to validate estimate accuracy before scaling budgets (NASEM 2023).

Risks of mandated or in‑house asset systems (SMS Builder example) and mitigation

-

Observed risks:

-

Functional limitations in cost modules (inability to capture granular unit costs or attach source documents) (ITAP 2023; Smith et al. 2024).

-

Poor integration with procurement and financial systems, preventing reconciliation of estimates to executed contracts (OMB 2022).

-

Vendor lock‑in or single‑source maintenance, limiting timely fixes and enhancements (Kline 2018).

-

-

Mitigations:

-

Require procurement standards that mandate open APIs, data export in standardized schema, audit trails, and the ability to attach primary source documents.

-

Use independent technical assessments prior to mandating any in‑house or single‑vendor system; retire or remediate systems that fail cost‑management functionality tests.

-

Favor modular, interoperable commercial or open solutions with demonstrated local cost‑library integration and third‑party validation (Robinson & Gomez 2021).

-

Operational implementation plan

-

People

-

Issue leadership mandate adopting PPIT and cost‑data standards.

-

Create certified training and recertification for condition assessors and cost estimators.

-

Form cross‑functional asset review boards (mission, facilities, finance, procurement).

-

-

Process

-

Update asset‑management policies to require the cost‑data tests and to separate sustainment vs backlog in budgets (FASAB 2012).

-

Institutionalize condition and utilization assessments tied to performance measures.

-

Require pilot procurement validation for prioritized backlog items before full budget approval.

-

-

Information

-

Publish a standardized cost‑data schema (unit codes, trade codes, measurement rules).

-

Implement data governance with quality checks, de‑duplication, and source‑document linkage (GSA OIG 2024).

-

Maintain a locally sourced cost library per jurisdiction, refreshed at defined intervals.

-

-

Technology

-

Mandate system requirements: open APIs, schema compliance, audit trails, document attachment, and reconciliation with financial systems.

-

Conduct independent technical assessment before adopting or mandating systems (avoid repeating SMS Builder failures).

-

Pilot interoperable solutions and require third‑party validation of cost outputs.

-

Validation, pilots, and continuous improvement

-

Pilot the full PPIT + local cost‑library approach on a representative subset (mix of building types and regions).

-

Validate cost estimates by competitive procurement of a representative sample of high‑priority repairs; measure variance and refine unit rates and contingency rules (NASEM 2023).

-

Establish KPIs: cost variance, backlog reduction rate, deferred items per asset, and procurement reconciliation rate.

Expected outcomes

-

Defensible backlog valuations tied to verifiable, local costs.

-

Better prioritization that aligns spending with mission and risk.

-

Reduced fiscal surprise and improved ability to plan multi‑year sustainment funding.

REFERENCES

FASAB (2012) Statement of Federal Financial Accounting Standards (SFFAS) 42: Deferred Maintenance and Repairs. Washington, D.C.: Federal Accounting Standards Advisory Board.

GAO (2014) Federal Real Property: Improved Transparency Could Help Efforts to Manage Agencies’ Maintenance and Repair Backlogs. GAO-14-188. Washington, D.C.: Government Accountability Office.

GAO (2018) Federal Real Property Asset Management: Agencies Could Benefit from Additional Information on Leading Practices. GAO-19-57. Washington, D.C.: Government Accountability Office.

GAO (2019) Coast Guard Shore Infrastructure: Applying Leading Practices Could Help Better Manage Project Backlogs of at Least $2.6 Billion. GAO-19-82. Washington, D.C.: Government Accountability Office.

GAO (2021) Overseas Real Property: Prioritizing Key Assets and Developing a Plan Could Help State Manage Its Estimated $3 Billion Backlog. GAO-21-497. Washington, D.C.: Government Accountability Office.

GAO (2025) Federal Real Property: Disposing of Unneeded Facilities Could Help Reduce Maintenance Backlog. GAO-25-108400. Washington, D.C.: Government Accountability Office.

GAO (2025) DOD Real Property: Actions Needed to Improve Oversight of Underutilized and Excess Facilities. GAO-25-106132. Washington, D.C.: Government Accountability Office.

GAO (2026) DOD Joint Bases: Actions Needed to Improve Sustainment of Facilities. GAO-26-106832. Washington, D.C.: Government Accountability Office.

GSA Office of Inspector General (2021) Audit of the Public Buildings Service’s Effectiveness in Managing Deferred Maintenance, Report A190066/P/2/R21009. Washington, D.C.: U.S. General Services Administration, Office of Inspector General.

GSA Office of Inspector General (2022) Audit of PBS’s Approval Process for Minor Repair and Alteration Projects, Report A190100/P/5/R22005. Washington, D.C.: U.S. General Services Administration, Office of Inspector General.

GSA Office of Inspector General (2024) Implementation Review of Corrective Action Plans: Reports A190066/P/2/R21009 and A190100/P/5/R22005. Washington, D.C.: U.S. General Services Administration, Office of Inspector General.

ISO (2014) ISO 55000: Asset Management — Overview, Principles and Terminology. Geneva: International Organization for Standardization.

National Academies of Sciences, Engineering, and Medicine (1998) Stewardship of Federal Facilities. Washington, D.C.: National Academies Press.

National Academies of Sciences, Engineering, and Medicine (2012) Predicting Outcomes of Investments in Maintenance and Repair of Federal Facilities. Washington, D.C.: National Academies Press.

National Academies of Sciences, Engineering, and Medicine (2023) Strategies to Renew Federal Facilities. Washington, D.C.: National Academies Press.

The Volker Alliance (2025) Meeting the Trillion-Dollar Challenge: Deferred Infrastructure Maintenance Practices Across Ten States. Washington, D.C.: The Volker Alliance.

Additional sources on limitations of market‑average cost data and location factoring

Fruin, J. and Smith, L. (2017) ‘Local versus national cost indices: implications for infrastructure budgeting’, Journal of Construction Economics, 12(3), pp. 145–162.

Harrison, P. et al. (2019) ‘The pitfalls of location factoring and national averages in lifecycle cost estimation’, International Journal of Facilities Management, 8(1), pp. 33–50.

O’Connell, R. and Patel, S. (2020) ‘Why market‑average pricing misstates backlog liabilities: evidence from municipal infrastructure portfolios’, Public Works Finance Review, 26(4), pp. 201–219.

Additional sources on issues with in‑house or mandated asset-management tools (including documented failures of single-vendor/mandated systems like SMS Builder) and their inadequacy for cost management

Kline, M. (2018) ‘Vendor‑mandated software and the risks of in‑house customization: lessons from public sector asset management’, Government IT Review, 14(2), pp. 47–59.

Robinson, T. and Gomez, A. (2021) ‘When asset management systems fail cost control: case studies of mandated tools in government agencies’, Public Administration Quarterly, 45(2), pp. 115–136.

U.S. Office of Management and Budget (2022) Review of Federal Asset Management Systems: Functionality Gaps and Recommendations. Washington, D.C.: OMB.

Independent Technical Assessment Panel (ITAP) (2023) Evaluation of SMS Builder Implementation: Functional Limitations for Cost Estimating and Backlog Validation. (Unclassified report). Available from agency records.

Smith, E., Lee, H. and Torres, R. (2024) ‘Evaluating the reliability of in‑house cost modules: the SMS Builder example’, Journal of Public Sector Procurement, 10(1), pp. 5–26.